Electric Vehicles are the major driving force of the sector

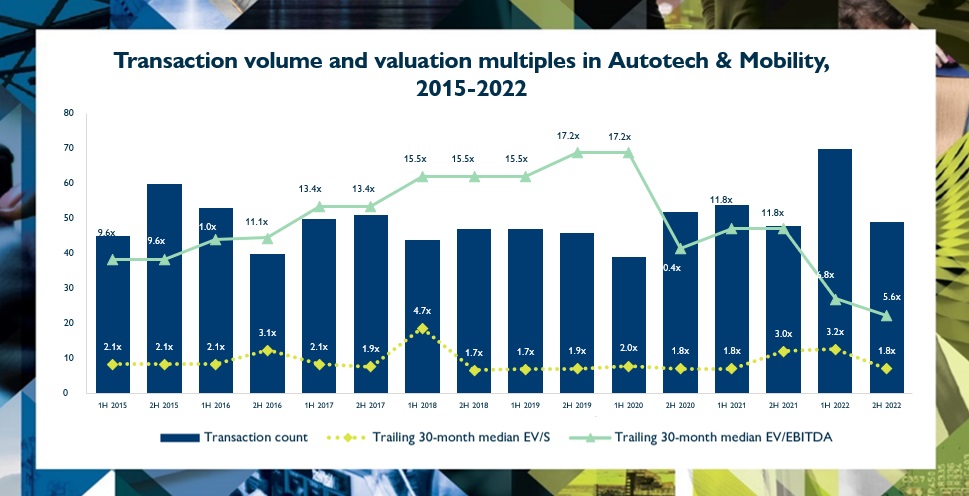

The latest global Autotech & Mobility M&A Market report from Hampleton Partners, the international M&A and corporate finance advisory firm for technology companies, reveals that 119 deals were struck in 2022, up 17 percent on 2021’s figure.

The rapid adoption in some markets of Electric Vehicles (EVs) has helped drive this record deal number.

Michel Annink, director, of Hampleton Partners, said: “2022 global EV sales grew by 55% year-on-year, reaching 10.5m, while global shipments of petrol and diesel-powered cars declined by 12% over that time. The EV-charging market also continues to boom with global investments in this segment in 2022 equal that of the previous five years combined.”

EV Charging Rollout

Although China was initially slow to adopt EVs, aggressive government policies and government incentives encouraged EV sales, achieving 29 percent of new car sales in 2022 vs. 15 percent in 2021. As a result, EV infrastructure has proliferated throughout big cities, supporting not only passenger cars, but also a significant proportion of electric buses, lorries, and two-wheelers.

By 2025, China hopes to have built enough EV infrastructure to handle up to 20 million EVs.

In the U.S. EV sales reached seven percent of new car sales in 2022 vs. four percent in 2021. However, EV charging port infrastructure is being rapidly rolled out with research projecting that they will reach parity with the 115k gas station numbers in the next few months[1].

Home charging is also growing with estimates that there were 9.6 million home EV chargers globally by the end of 2022[2].

Top autotech acquirers – past 30 months

Globally there have been 236 active acquirers in the autotech and mobility sector over the past 30 months, 33 of which made more than one acquisition. The three most prolific acquirers and their three most recent deals are:

Imaweb 2000 – 7 acquisitions: Custeed SAS – CRM SaaS for automotive retail; FordonsData Nordic – automotive dealer management software; Stieger Software – automotive dealership management software.

Envase – 4 acquisitions: GeoStamp Industries – geospatial location data & analytics SaaS; Infosite Technologies – Trucking dispatch SaaS & software; DrayMaster Enterprise rate https://marylebonemarketing.

JD Power – 4 acquisitions: Tail Light – automotive finance and insurance (F&I) menu and reporting SaaS; Superior Integrated Solutions – automotive F&I SaaS; Inventory Command Center – SaaS for auto businesses.

Download the full Hampleton Partners’ Autotech & Mobility M&A Market Report 1H2023, which includes an extensive section on Electric Vehicle headlines, trends, and key transactions, plus deal volume and valuations on the Enterprise Applications; Internet Commerce & Content; Embedded Software & Systems and Mobility & Fleet Management segments: https://www.hampletonpartners.

[1] & [2]. Source: Bloomberg New Energy Finance