Consumers Can Increase Their Credit Score Knowledge by Taking the

Credit Score Quiz (CreditScoreQuiz.org)

NOTICE: PRESS TELECONFERENCE TODAY

June 10, 2019 12:00

NOON EASTERN

CALL IN NUMBER: 800-247-5110 PASSCODE:

CFACALL

WASHINGTON–(BUSINESS WIRE)–The ninth annual credit score survey, released today by the Consumer

Federation of America (CFA) and VantageScore Solutions, LLC, shows that

consumer knowledge about credit scores is at the lowest level in the

past eight years. On most knowledge questions (as the enclosed table and

charts show), correct scores declined by more than ten percentage

points, and sometimes by more than 20 percentage points. For example:

-

78% of respondents in 2012, but only 62% in 2019, correctly indicated

that people have more than one credit score. -

85% in 2012, but only 66% in 2019, correctly answered that keeping a

low credit card balance helps raise a low credit score or maintain a

high one.

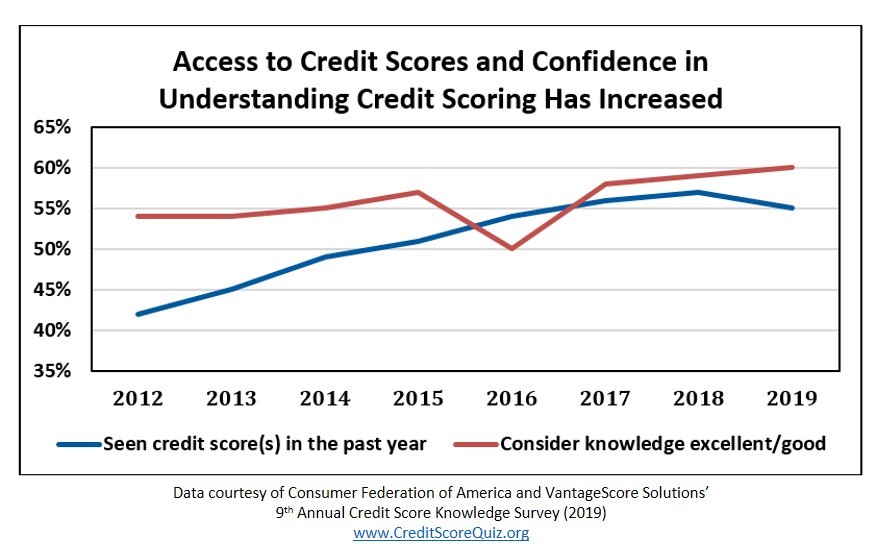

However, in the same period, the proportion of respondents who said they

considered their knowledge of credit scores excellent or good rose from

54% to 60%.

“Consumers know less about credit scores but think they know more,” said

Stephen Brobeck, CFA senior fellow. “Taking our online credit score quiz

provides an easy way for consumers to update their credit score

knowledge,” he added. More than 230,000 individuals have taken the Credit

Score Quiz, developed and maintained by CFA and VantageScore.

“We are pleased that many consumers now have free access to their credit

scores, but consumers must also take advantage of all the additional

information about credit scores and credit files in order to make better

credit decisions,” said Barrett Burns, president and CEO of VantageScore

Solutions.

Consumer knowledge levels may have deteriorated, in part, because of

improvements in the overall economy and consumers’ financial condition.

In 2012, large numbers of Americans faced challenging credit card and

mortgage debts, so consumers may have been especially concerned about

credit scores. Since then, as the nation’s economy and family finances

recovered, and as consumers reduced unsustainable credit card and

mortgage debts, consumers may have felt that it was less important to

fully understand credit scores. Reports of increases in average credit

scores nationwide may also have lessened people’s feelings of financial

vulnerability and the need to fully learn about their scores and its

impact.

Despite overall rising score levels – now averaging 680 according to

Experian – a large minority of consumers have fair or poor scores (below

670). Low scores can especially harm these people by:

- Denying them access to needed credit.

-

Increasing the costs of consumer and mortgage credit they can obtain.

Subprime auto loans will likely cost several thousand dollars more,

and subprime mortgage loans can cost over ten

thousand dollars more, compared to conventional loans. -

Increasing deposits required by utilities and cell phone companies to

obtain service.

Low credit scores also are an indicator that people may have difficulty

obtaining a job. While credit scores themselves are not used by

employers, the credit reports the scores are based on are frequently

utilized. “Those with low credit scores should be aware that they are at

risk not only for paying higher costs for credit and utility services,

but may also struggle to obtain a good job with which to afford those

higher costs,” noted CFA’s Brobeck.

While consumers’ knowledge of their actual credit scores has declined

overall, the latest survey shows large majorities of consumers did

correctly answer key knowledge questions related to important facts:

-

Mortgage lenders and credit card issuers use credit scores (83% and

82% respectively). - Missed payments are used in calculating credit scores (86%).

-

Making all loan payments on time helps a consumer raise a low credit

score or maintain a high one (87%).

However, significant minorities of respondents did NOT

know other key facts, for example:

- Cell phone companies might use credit scores in pricing services (41%).

-

Borrowing from a 401k retirement account or paying a parking ticket

late will not lower your credit scores (30% and 22% respectively). -

Opening several credit card accounts at the same time might lower

scores (38%). - Frequently checking credit scores will not lower their scores (38%).

-

Checking the accuracy of one’s credit reports is very important (33%).

Lenders may have provided inaccurate information or failed to supply

accurate information to credit bureaus; thus, the bureaus may have

made mistakes such as adding information to the wrong file of a person

with the same name.

In brief, consumers can raise their credit scores or maintain high

scores by:

-

Consistently making loan payments on time every month. A late payment

may lower one’s credit scores by dozens of points. -

Using a small portion of the credit available on a credit card. In

general, the higher the percentage of credit line that is drawn down,

the lower one’s credit scores. -

Paying down credit card debt rather than just shifting it to another

credit card or to a home equity loan. -

Regularly checking one’s credit reports to make sure they are

error-free. This can be done for free annually by going to annualcreditreport.com

or by calling 800-322-8228.

The survey was conducted by the Engine Telephone CARAVAN survey, who on

April 25-28, 2019, interviewed 1,002 representative adult Americans by

landline or cell phone. The survey’s margin of error is plus or minus

three percentage points.

Please see a detailed overview of the historical results for the Credit

Score Knowledge Survey at www.VantageScore.com/CreditScoreKnowledge19.

Percentage of Respondents with Correct Answers

| Topic | Correct Answer(s) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |||||||||

| Who uses scores? | Credit card issuers | 90 | 89 | 88 | 89 | 87 | 85 | 85 | 82 | |||||||||

| Mortgage lenders | 94 | 87 | 87 | 88 | 88 | 85 | 84 | 83 | ||||||||||

| Landlords | 73 | 69 | 70 | 72 | 70 | 67 | 71 | 65 | ||||||||||

| Cell phone companies | 66 | 61 | 61 | 62 | 68 | 59 | 58 | 59 | ||||||||||

| Home insurance | 71 | 64 | 67 | 66 | 66 | 62 | 61 | 58 | ||||||||||

| What factors are used to calculate scores? | Miss payments | 94 | 90 | 92 | 92 | 91 | 91 | 86 | 86 | |||||||||

| High balances on credit cards | 89 | 85 | 87 | 86 | 85 | 86 | 81 | 78 | ||||||||||

| Personal Bankruptcy | 90 | 86 | 87 | 88 | 86 | 85 | 79 | 71 | ||||||||||

| Who collects info for scores? | Credit bureaus | 75 | 71 | 72 | 70 | 68 | 64 | 68 | 66 | |||||||||

| Do consumers have more than one score? | More than one score | 78 | 71 | 72 | 70 | 69 | 67 | 68 | 62 | |||||||||

| When are lenders required to disclose a credit score? | When a loan is rejected | 79 | 76 | 76 | 78 | 78 | 78 | 67 | 64 | |||||||||

| After loan application | 80 | 73 | 75 | 77 | 75 | 75 | 62 | 62 | ||||||||||

| When a consumers doesn’t receive the best terms | 70 | 65 | 66 | 67 | 69 | 66 | 56 | 54 | ||||||||||

| How do you raise a low score/maintain a high credit score? | Make loan payments on time | 97 | 94 | 95 | 97 | 95 | 96 | 89 | 87 | |||||||||

| Keep credit card balances under 25% | 85 | 74 | 76 | 78 | 78 | 80 | 72 | 66 | ||||||||||

| Avoid opening several accounts at once | 83 | 72 | 72 | 72 | 73 | 74 | 66 | 62 | ||||||||||

| Is it important to check credit report accuracy? | Very important | 82 | 74 | 72 | 74 | 73 | 68 | 67 | 67 | |||||||||

| What agency is best for resolving a complaint? | CFPB | NA | NA | 74 | 73 | 72 | 73 | 68 | 66 | |||||||||

| Are credit repair companies usually or never helpful? | Never | 46 | 57 | 55 | 53 | 54 | 47 | 44 | 44 | |||||||||

| Average score for key knowledge questions | 80 | 75 | 76 | 76 | 76 | 74 | 70 | 67 | ||||||||||

| Seen credit score(s) in the past year | 42 | 45 | 49 | 51 | 54 | 56 | 57 | 55 | ||||||||||

| Consider knowledge excellent/good | 54 | 54 | 55 | 57 | 50 | 58 | 59 | 60 | ||||||||||

The

Consumer Federation of America is an association of more than

250 non-profit consumer groups that, since 1968, has sought to advance

the consumer interest through research, education, and advocacy.

VantageScore

Solutions, initially developed by America’s three national

credit reporting companies (CRCs) – Equifax, Experian, and TransUnion –

is the independently managed company behind the VantageScore credit

scoring model.

Contacts

Jack Gillis, 202-939-1018

Jeff Richardson, VantageScore Solutions

203-363-2170