Sends Letter to Mack-Cali Shareholders Outlining Decades of Value

Destruction Overseen by Deeply Entrenched Board

Reiterates Need to Repair Mack-Cali’s Broken

Structure by Exploring Strategic Alternatives to Maximize Shareholder

Value

Urges Mack-Cali Shareholders to VOTE the GOLD

Proxy Card FOR the Election of Bow Street’s

Four Highly-Qualified, Independent Director Nominees

NEW YORK–(BUSINESS WIRE)–Bow Street LLC (“Bow Street”), a New York-based investment firm that

beneficially owns approximately 4.5% of the outstanding shares of common

stock of Mack-Cali Realty Corporation (“Mack-Cali” or the “Company”)

(NYSE: CLI), announced today that it has filed a definitive proxy

statement with the Securities and Exchange Commission for the election

of four highly-qualified, independent director nominees to Mack-Cali’s

Board of Directors (the “Board”) in connection with the Company’s 2019

Annual Meeting of Shareholders to be held June 12, 2019.

Additionally, Bow Street is sending a letter to its fellow Mack-Cali

shareholders outlining the decades-long value destruction overseen by

the Company’s deeply entrenched Board as well as Bow Street’s belief

that new independent directors and significant structural change are

required to unlock value for all shareholders.

Akiva Katz, Managing Partner of Bow Street, said, “Decades of

mismanagement and missed opportunities by its Board have left Mack-Cali

in a dangerous and untenable position. Mack-Cali’s persistently wide

discount to NAV is currently and historically amongst the widest in the

REIT universe; the Company’s efforts to close this discount have failed,

causing shareholders to suffer bottom quartile stock performance over

any appreciable multiyear period. We believe Mack-Cali’s value will

never be realized in its current broken structure, and once again urge

the Board to launch a process to explore all strategic alternatives to

maximize shareholder value.”

Howard Shainker, Managing Partner of Bow Street, continued, “For the

last several months, we have endeavored to engage constructively with

the Board, and are deeply disappointed by its perfunctory dismissal of

our proposal and refusal to explore any other alternatives. This Board’s

actions are consistent with its reputation for entrenchment and

resistance to change. Accordingly, we are nominating four

highly-qualified, independent director candidates to ensure

transparency, fairness and good governance prevail over stubborn

intransigence. If elected, our nominees will bring fresh perspective,

skills and a governance-centric approach to a Board desperately in need

of independence.”

The full text of the letter is below.

May 1, 2019

Dear Fellow Mack-Cali Shareholder:

Fifteen years is a long time.

Over the last fifteen years, global asset values – and the value of New

York Metro area real estate in particular – have surged. In hindsight,

Mack-Cali Realty Corporation (“Mack-Cali,” “CLI,” or “the Company”)

should have been well positioned to capitalize on this pending boom. As

proudly detailed in the Company’s 2004 Annual Report, Mack-Cali owned a

portfolio of $4.16 billion1 of real estate assets located

primarily in the Northeast, had a balance sheet it described as “one of

the strongest in the industry,” and enjoyed a reputation “as one of the

country’s leading real estate investment trusts.”2

However, while a dollar invested in the benchmark MSCI US REIT Index

(RMZ) at its inception in 2005 is worth $2.613 today, that

very same dollar invested in Mack-Cali stock over the same period has

declined in value, and is now worth only 92 cents3

(inclusive of dividends). Despite presiding over these

abysmal results, the majority of Mack-Cali’s current directors –

including Chairman William Mack – have served on the Company’s Board of

Directors (the “Board”) for over fifteen years. In its proxy statement

filed on April 29th, Mack-Cali is once

again urging shareholders to re-elect these directors to the Board –

essentially asking you to validate and perpetuate their track record of

value destruction and poor governance.

We Own a Meaningful Stake in Mack-Cali; We Are Focused on

Maximizing Value for All Shareholders

Bow Street LLC (“Bow

Street” or “we”) manages funds that beneficially own 4.5% of Mack-Cali.

Founded in 2011, Bow Street is a New-York based investment manager that

partners with institutional investors and family offices globally to

invest opportunistically across asset class, geography and industry. We

own long-duration assets in both the public and private markets, and

this proxy filing is our first such submission since Bow Street’s

founding over eight years ago.

In Mack-Cali’s public communications, the Board suggests we are working

to force the Company’s sale at a so-called “fire sale” price4.

Nothing could be further from the truth. We have explicitly called for:

i) the launch of a fulsome process to analyze all

prospective value maximizing strategic alternatives, and

ii) the nomination of four new independent

directors to replace some of the longest tenured members of Mack-Cali’s

entrenched Board, which has overseen more than two decades of value

destruction.

As significant shareholders, we are motivated to maximize the value of

Mack-Cali’s shares for all investors. Let

us be clear: we believe Mack-Cali should indeed be sold – to the highest

bidder in a robust, transparent auction process.

Mack-Cali is Trapped – Its Value Will Never be Realized in its

Current Broken Structure

Decades of mismanagement, missed

opportunities, and myriad conflicts have left Mack-Cali in a dangerous

and untenable position. Despite repeated promises by management and the

Board to de-lever, Mack-Cali’s debt levels have risen consistently over

the years and the Company remains amongst the most highly levered of all

publicly-traded REITs5. This leverage issue is unlikely to be

resolved anytime soon. Instead, Mack-Cali will be severely cash-flow

constrained for the foreseeable future, hampered by significant vacancy

in its commercial portfolio and its highly capital-intensive residential

development platform.

Mack-Cali is trapped, lacking the required

financial resources to maximize value for either its office portfolio or

its growing residential business. We believe that the value

of the Company’s underlying assets will never be realized in the public

markets in its current broken structure. The market clearly shares our

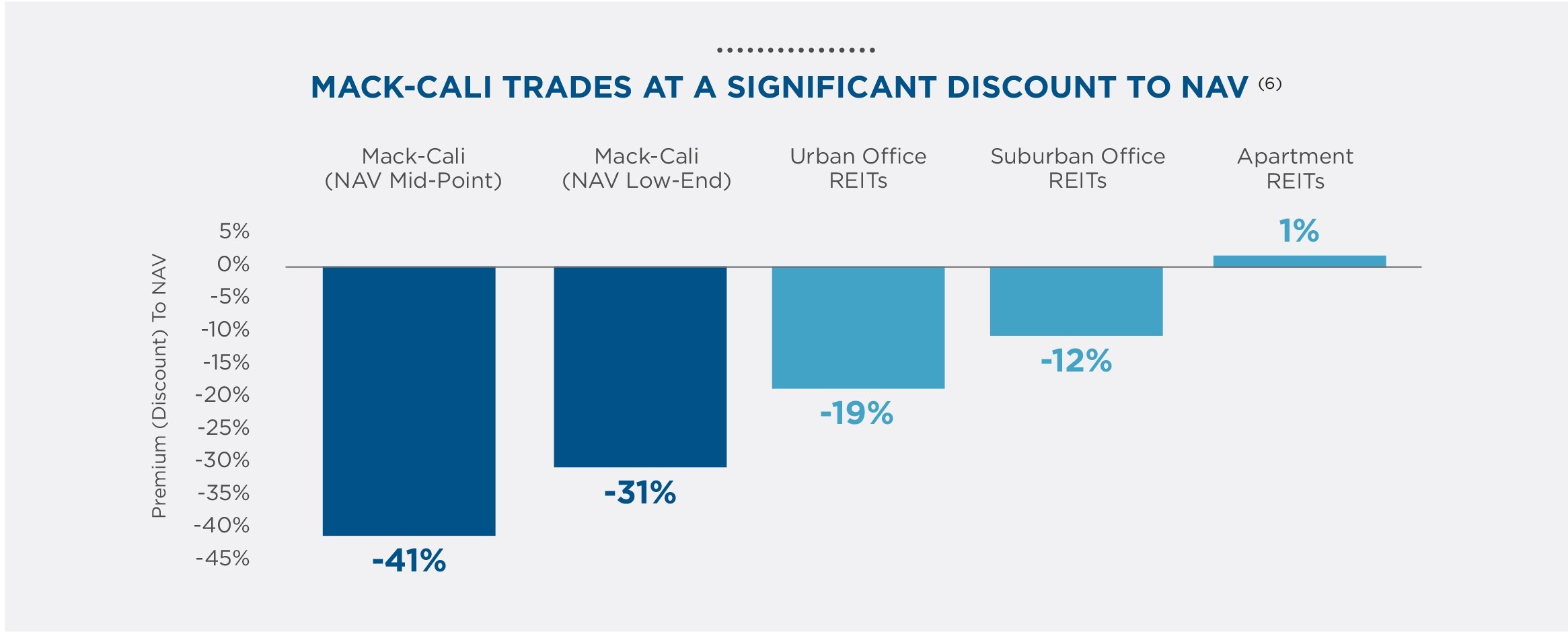

perspective, as evidenced by:

(i) the Company’s persistently wide discount to net asset value

(“NAV”), currently and historically amongst the widest in the REIT

universe6;

(ii) the lack of a single “Buy” recommendation amongst the eight

Wall Street brokerage analysts7 covering the stock; and

(iii) a share price that has stagnated for decades.

See chart detailing Mack-Cali’s NAV trading discount to peers.

We Made a Value Creative Proposal; Mack-Cali’s Board Promptly

Rejected It Without Proper Inquiry

Consequently, we

proposed a transaction that we believe addresses Mack-Cali’s issues,

delivering value of up to $27-$29 per share to shareholders.8

Specifically, our proposed transaction contemplates the acquisition of

Mack-Cali’s corporate shell, followed by a subsequent distribution of

the Company’s multi-family residential assets to shareholders. Taxes and

other transaction friction – cited by the Company on multiple occasions

as material impediments to effectuating the transaction – would be Bow

Street’s liabilities, not those of Mack-Cali shareholders.

The Board could have easily clarified the details of our transaction

through meaningful inquiry regarding valuation, structure, tax or other

implications for shareholders. However, rather

than conduct proper diligence, the Company quickly issued a misleading

press release rejecting the proposal. Concurrently,

Mack-Cali offered Bow Street two board seats in exchange for our

silence, explicitly refusing to consider any material changes to

corporate strategy.

The Board’s Behavior is Par for the Course; What Other Offers Have

Been Similarly Rejected?

Unfortunately, as longtime

Mack-Cali shareholders know all too well, these actions are broadly

consistent with this entrenched Board’s well-earned reputation for

discouraging prospective suitors. As recently as last September, Bloomberg

News reported that Mack-Cali may have received and rejected a “fully

financed bid at a significant premium.”9 In the weeks since

our investment in Mack-Cali has been made public, we have heard this

very same story repeated by numerous rebuffed acquirers.

To be clear, your vote at Mack-Cali’s 2019 Annual Meeting of

Shareholders is not about our offer, but rather about all

prospective value-creative solutions – none of which this Board can

afford to ignore given the abysmal status quo. We are therefore

calling on the Board to immediately launch a process whereby all

strategic alternatives are evaluated – including our own – to maximize

value for all shareholders.

Mack-Cali’s Underperformance is Undeniable – Chairman Mack and His

Board Have Failed Shareholders

A majority of Mack-Cali’s

current directors have served on the Board for fifteen years or longer,

overseeing the Company’s legacy of value destruction. The Company’s

share price has consistently trailed its peers, resulting in bottom

quartile performance across 3-, 5-, 10-, 15-, and 20-year periods10.

Over the last fifteen years, under Chairman Mack’s leadership,

Mack-Cali shareholders have seen:

- their dividend cut by nearly 70%;

-

Funds From Operations per share decline by

50%; -

debt load increase by $700 million;

and - the value of their shares decline by 50%.

Absent a transformational transaction, we believe Mack-Cali shares will

continue to languish, extending this underperformance.

See chart detailing Mack-Cali’s material underperformance against

relevant peer indices over the last several decades.

The Status Quo is Broken; An Exploration of Strategic Alternatives

is Required to Unlock Value

Bow

Street has nominated four highly-qualified, independent directors to

refresh the Board and ensure that transparency, fairness and good

governance prevail over stubborn intransigence. Our

nominees bring unique perspectives and important skills to a Board

desperately in need of independence. Importantly, our nominees also

share a commitment to strong shareholder governance, and have the

fiduciary constitution required to resist Chairman Mack’s legacy of

dismissing value-creative proposals.

If elected, we anticipate our independent nominees will work to ensure a

full exploration of strategic alternatives. A robust auction process for

Mack-Cali should attract a wide swath of buyers given the Company’s

attractive assets, resulting in an outcome far

superior and less risky than entrusting the Company to this Board for

another fifteen years.

Join us in VOTING THE GOLD PROXY CARD

to prioritize Board independence and encourage the Mack-Cali Board to

explore all strategic alternatives to create value for all Mack-Cali

shareholders.

Respectfully,

|

Akiva Katz

Managing Partner |

Howard Shainker

Managing Partner |

|

Your Vote Is Important, No Matter How Many or How Few Shares |

| Please vote today by telephone, via the Internet or |

|

by signing, dating and returning the enclosed GOLD proxy |

|

Simply follow the easy instructions on the GOLD proxy card. |

| If you have questions about how to vote your shares, please contact: |

|

INNISFREE M&A INCORPORATED |

|

Shareholders May Call Toll-free: (877) 800-5182 |

|

Banks and Brokers May Call Collect: (212) 750-5833 |

|

REMEMBER: |

|

Please simply discard any White proxy card that you may receive |

|

|

About Bow Street LLC

Founded in 2011, Bow Street is a New York-based investment manager that

partners with institutional investors and family offices globally to

invest opportunistically across public and private securities.

|

1 Rental property before accumulated depreciation and amortization as listed on page 42 of Mack-Cali’s 10-K, filed with the SEC on March 3, 2005. |

| 2 Mack-Cali 2004 Annual Report Letter To Stockholders. |

|

3 Total return with dividends reinvested in index per Bloomberg; measured from 6/20/2005 to 3/15/2019 (closing date prior to Mack-Cali press release discussing Bow Street’s proposal). |

| 4 Mack-Cali Press Release, issued on April 29, 2019. |

|

5 Mack-Cali net debt / EBITDA of 9.3x (Q4 2018 Supplement) compares to urban office peer average of 6.7x, suburban office average of 6.6x, and multifamily average of 5.8x per Citi Research “the Hunter Express and Lodging Valuation Tool”, 3/18/2019. |

|

6 Mack-Cali NAV calculated using management guidance as of Q4 2018 Supplement (stock price as of 3/15/2019); peer / industry REIT NAV levels using Citi Research “the Hunter Express and Lodging Valuation Tool” as of 3/18/2019. |

|

7 Bloomberg, two analysts (Stifel and BTIG) recently upgraded CLI; however, these upgrades were catalyzed by Bow Street’s proposal rather than the Company’s prospects. |

|

8 Please see our attached proxy statement and our press release, dated April 16, 2019, for details. |

|

9 Scott Deveau and Gillian Tan, “Litt Says Mack-Cali |

|

10 Using public REITs that were public throughout |

Important Information

Bow Street LLC (“Bow Street”), A. Akiva Katz, Howard Shainker, Alan R.

Batkin, Frederic Cumenal, MaryAnne Gilmartin, and Nori Gerardo Lietz

(collectively, the “Participants”) have filed with the Securities and

Exchange Commission (the “SEC”) a definitive proxy statement and

accompanying form of proxy to be used in connection with the

solicitation of proxies from shareholders of Mack-Cali Realty

Corporation (the “Company”). All shareholders of the Company are advised

to read the definitive proxy statement and other documents related to

the solicitation of proxies by the Participants, as they contain

important information, including additional information related to the

Participants. The definitive proxy statement and an accompanying proxy

card is being furnished to some or all of the Company’s shareholders and

is, along with other relevant documents, available at no charge on the

SEC website at http://www.sec.gov/

or from the Participants’ proxy solicitor, Innisfree M&A Incorporated.

Information about the Participants and a description of their direct or

indirect interests by security holdings is contained in the definitive

proxy statement on Schedule 14A filed by Bow Street with the SEC on May

1, 2019. This document is available free of charge from the sources

indicated above.

Disclaimer

This material does not constitute an offer to sell or a solicitation of

an offer to buy any of the securities described herein in any state to

any person. In addition, the discussions and opinions in this press

release are for general information only, and are not intended to

provide investment advice. All statements contained in this press

release that are not clearly historical in nature or that necessarily

depend on future events are “forward-looking statements,” which are not

guarantees of future performance or results, and the words “anticipate,”

“believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,”

and similar expressions are generally intended to identify

forward-looking statements. The projected results and statements

contained in this press release that are not historical facts are based

on current expectations, speak only as of the date of this press release

and involve risks that may cause the actual results to be materially

different. Certain information included in this material is based on

data obtained from sources considered to be reliable. No representation

is made with respect to the accuracy or completeness of such data, and

any analyses provided to assist the recipient of this presentation in

evaluating the matters described herein may be based on subjective

assessments and assumptions and may use one among alternative

methodologies that produce different results. Accordingly, any analyses

should also not be viewed as factual and also should not be relied upon

as an accurate prediction of future results. All figures are unaudited

estimates and subject to revision without notice. Bow Street disclaims

any obligation to update the information herein and reserves the right

to change any of its opinions expressed herein at any time as it deems

appropriate. Past performance is not indicative of future results.

Contacts

Media Contacts

Gasthalter & Co.

Jonathan

Gasthalter/Amanda Klein

(212) 257 4170

Investor Contacts

Innisfree M&A Incorporated

Scott

Winter/Gabrielle Wolf

(212) 750 5833